TSMC reportedly adds outside packaging capacity as buyers fund 2029 plants

Zero One Investment Research Daily Intelligence Brief, August 5, 2026

TSMC reportedly adds outside packaging capacity as buyers fund 2029 plants

Top Market Signals

TSMC reportedly adds outside capacity at its tightest packaging step

TSMC (2330 TT) reportedly plans to expand external chip-on-wafer (CoW) bonding capacity, the most strained step inside its CoWoS (chip-on-wafer-on-substrate) advanced packaging flow, through outside assembly and test houses led by ASE Technology (3711 TT), according to Korea's Electronic Times as reported by Liberty Times. If accurate, the plan would add a new external source at scale while TSMC continues expanding its own lines. TSMC has not confirmed the report.

This changes the boundary between the two halves of CoWoS. TSMC has licensed the wafer-on-substrate (WoS) step, which joins the interposer to the main substrate, to ASE, Amkor and SPIL for years. Chip-on-wafer, which bonds the logic die and the memory stacks onto the interposer, stayed almost entirely in house because it gates yield, and the report describes prior CoW outsourcing as very limited.

The OSATs invited to take CoW work are already building lines and are in purchase order negotiations with Korean materials, component and equipment suppliers. Liberty Times names laser processing, wafer and interposer dicing, and bonding tools as the core of that equipment spend, which is why Korean back-end suppliers are the near-term beneficiaries alongside the Taiwanese packagers.

TSMC is expanding its own packaging capacity at the same time, so OSAT equipment orders add to the industry's tool demand. Investment amounts have not been disclosed. The capex guidance the OSATs give at their next results is what would size it.

Linked stocks: 2330 TT, 3711 TT, AMKR US

Substrate buyers pull 2029 plant plans forward

NVIDIA (NVDA US), AMD (AMD US) and the hyperscalers have locked ABF (Ajinomoto Build-up Film) substrate long-term agreements out to 2028 and still cannot cover their requirements, so they are asking Taiwanese substrate makers to bring 2029 and 2030 expansion plans forward, DigiTimes reports. Customers are consigning equipment, paying tool prepayments and sharing construction costs in exchange for priority supply.

That is the same model that ran in 2021 and 2022, when prepayments, long contracts and joint plant builds pushed order visibility out several years. Demand reversed in 2H22, customers cut orders sharply, and the capacity added in 2022 and 2023 left Taiwanese substrate makers in a trough for close to three years.

The current round is already visible in capex. Unimicron (3037 TT) raised 2026 capex to NT$53.7bn for its Guangfu second plant and Yangmei second and third plants. Kinsus (3189 TT) added NT$19.6bn of project capex for the Yangmei K6C and D plants and is scouting land for K7 and K8. Nan Ya PCB (8046 TT) capex is rising off a trough. AMD chief executive Lisa Su committed more than US$10bn of expanded Taiwan investment to seed a local elevated fanout bridge (EFB) 2.5D packaging ecosystem as a second route alongside TSMC's CoWoS, with all three substrate makers on the partner list.

Japan is showing the same demand pressure. Ibiden (4062 JT) raised its full-year forecast after IC substrate demand ran far ahead of plan, and its shares rose 24.5% on 5 Aug. Ibiden's read-across reinforces the case for accelerated Taiwanese capacity.

Pricing carries the shortage. ABF and BT substrate quotes have been rising about 8% a quarter, with 2H26 increases larger than 1H26, and DigiTimes reports ABF increases will now run ahead of BT because high performance compute demand concentrates there. Shortages of T-glass fiberglass cloth cap how fast new capacity can come on. What separates this cycle from 2022 is whether the prepayment and profit-guarantee terms actually hold when order growth slows, and that is not testable until it does.

Linked stocks: 3037 TT, 3189 TT, 8046 TT, NVDA US

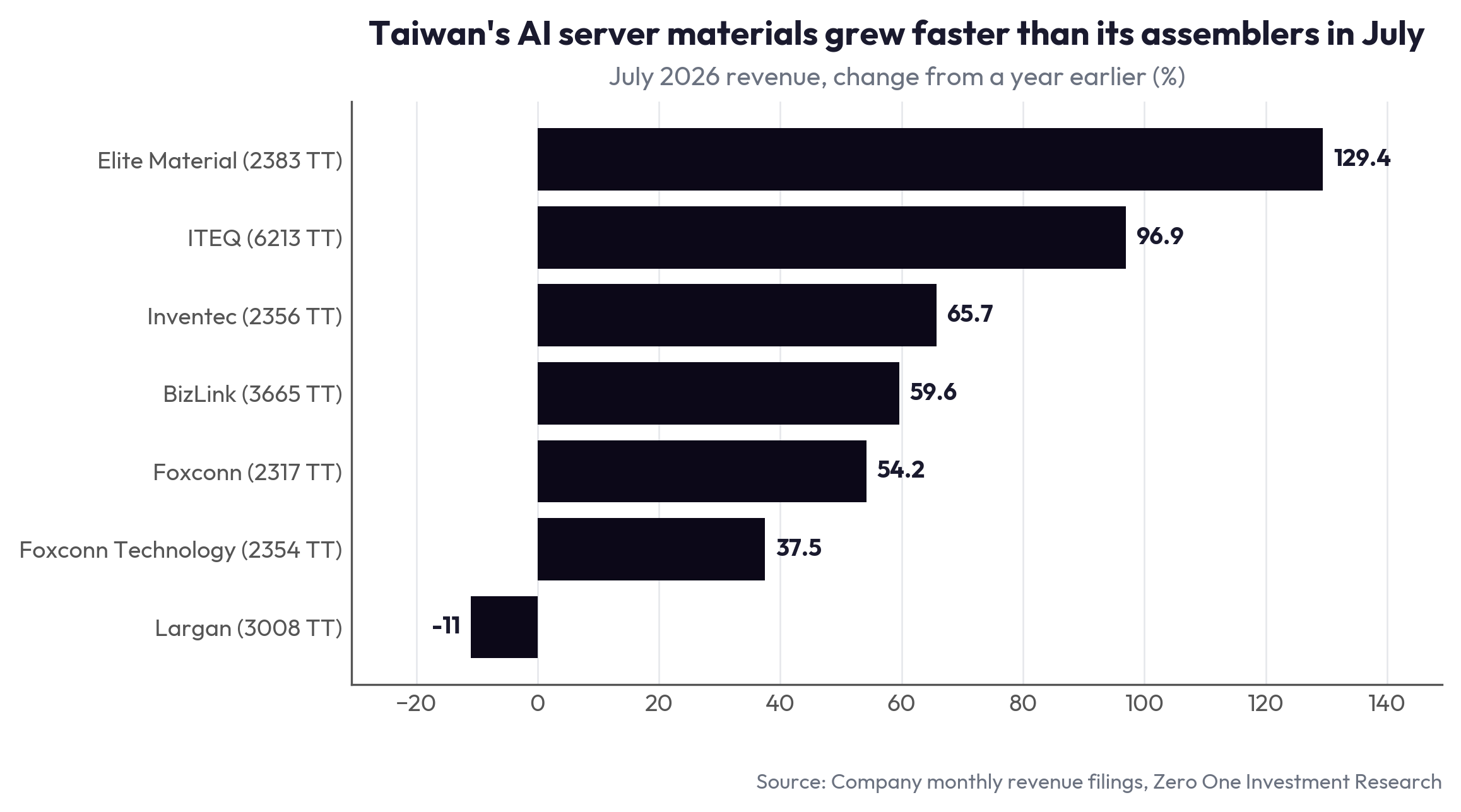

Foxconn clears NT$900bn in a single month

Foxconn (2317 TT) reported July revenue of NT$946.51bn, up 15.18% MoM and 54.19% YoY, its first month above the NT$900bn mark. Revenue for the year to July reached NT$5.589tn, up 37.89% and a record for the period.

All four product lines grew YoY. Cloud and networking products led on AI pull-in, computing products improved on better order momentum, components and other rose on related parts and other income, and smart consumer electronics grew as well.

Management guided 3Q26 to grow both QoQ and YoY, citing continued growth in AI rack shipments and the seasonal 2H ramp in information and communications products, while naming global political and economic conditions as the variable it is still watching. Whether the AI rack mix is carrying group margin as well as revenue, and what that implies for fellow server assemblers Wistron (3231 TT) and Wiwynn (6669 TT), is what the 13 Aug 2026 results release will show.

Linked stocks: 2317 TT, 3231 TT, 6669 TT, NVDA US

Wistron expects networking business to grow more than tenfold

Wistron (3231 TT) expects its networking business to grow more than 10 times this year after qualifying into North America's largest networking company, which in turn supplies cloud service providers, president Jeff Lin said at the 4 Aug results call. Gross margin and operating margin on that business are both running well, and further new customers are in discussion.

The customer mix is the part that changed. Wistron has won new enterprise and CSP accounts covering L10 and L11 assemblies, work that had largely sat with sister company Wiwynn (6669 TT). Lin said AI server demand will be stronger in 2H26 than in 1H26 and that customer forecasts already extend the strength into 1H27, with some accounts still buying GB300 while others move to Vera Rubin.

The half-year numbers underneath that: 1H26 revenue of NT$1.74tn, up 94% YoY, net profit of NT$24.46bn and EPS of NT$7.78. The board approved a global depositary receipt issue of up to 250m shares and NT$17.48bn of new investment across Taiwan, the United States and Vietnam.

Lin expects 2H26 PC shipments to fall 15% after customers pulled orders forward on memory price increases, though he said revenue need not fall with them because end prices are rising. On AI servers he argued memory inflation does not change orders, because that demand is not discretionary. The gating item is whether switch gross margin holds as the volume scales.

Linked stocks: 3231 TT, 6669 TT, NVDA US

AMD doubles data center revenue; guide misses elevated expectations

AMD (AMD US) reported 2Q26 revenue of US$11.54bn, up 50% YoY, with data center revenue up 107% to US$6.72bn and data center operating income of US$2.10bn against a US$155m loss a year earlier. GAAP gross margin reached 54%, up 14 points YoY. Shares fell about 9% after the print.

The guide explains the reaction. AMD's 3Q26 revenue outlook of US$13.0bn plus or minus US$0.3bn sits above the LSEG analyst consensus of US$12.52bn, but TechNews reports parts of the market had lifted their own bar to US$14bn. The shares had roughly tripled over the prior year, which is what pushes expectations above the published consensus.

Management's forward numbers run larger than the quarterly guide implies. Lisa Su said data center revenue will double again in 2027, that 2H26 server revenue will grow more than 80% YoY, and that an outside estimate of roughly US$30bn for 2027 Instinct revenue may be too low. AMD also put the 2030 server CPU market at about US$220bn, against an estimate of more than US$100bn today.

The first Helios rack-scale systems ship this quarter to Meta, OpenAI and Oracle, with volume in 4Q26. Gaming revenue fell 31% YoY to US$779m, which Su attributed partly to higher industry-wide component costs feeding into graphics card prices. Whether the 2027 doubling is deliverable depends on the Instinct supply AMD can actually secure, and that is the number to press management on next quarter.

Linked stocks: AMD US, NVDA US, 2330 TT

The memory shortage is refilling Samsung's logic fabs

Samsung Electronics (005930 KS) expects its foundry utilization to reach 100% in 2H26, up from an estimated 70% to 80% now, according to Korean market reports carried by TechNews. The division ran below 50% utilization from 2024, so full loading is the mechanism that would end its losses, given how much of foundry cost is fixed.

HBM4 is the largest reason. The sixth generation of high bandwidth memory (HBM) puts its base die on a 4nm logic process, which converts the memory shortage directly into foundry loading. Demand from cloud service providers and AI and high performance computing customers for 2nm adds to it, with Broadcom among the accounts still in discussion.

Advanced nodes are expected to exceed 50% of Samsung foundry revenue in 2026, and AI and HPC revenue to rise from a high-teens share in 2025 to more than 30% this year. The report puts a swing to profit at the non-memory division as early as 3Q26 and at the latest 4Q26, faster still if wafer price increases land on top of normalized utilization.

Yield is the gate. Samsung's 2nm yield is estimated at about 60% and the view cited is that large volume contracts require it stable above 70%. Second generation 2nm (SF2P) mobile products enter production in 2H26, the first Taylor, Texas fab is on track to start production by end 2026, and a second Taylor fab is due to break ground this year for 2030 output. Customer conversions from evaluation to mass production are what would confirm the turn.

Linked stocks: 005930 KS, 2330 TT, AVGO US

Samsung and SK Hynix reportedly weigh Chinese etch tools as a hedge

Samsung Electronics (005930 KS) and SK Hynix (000660 KS) have been evaluating chipmaking equipment from China's Advanced Micro-Fabrication Equipment (AMEC, 688012 CH) for their China fabs as a hedge against tighter US export controls, Reuters reported citing three people familiar with the matter. Samsung told Reuters it has not tested AMEC equipment at its China plants and has never considered doing so; SK Hynix declined to comment.

Two of the sources said testing of AMEC etch equipment began about two years ago, when it was unclear whether Washington would keep permitting the two companies to import US chipmaking equipment into China. No decision to expand adoption has been made.

The reported evaluations show how controls written to slow China's domestic semiconductor build could open a route for a Chinese toolmaker into foreign-owned fabs on Chinese soil. The evidence remains contested because Samsung denies testing the equipment. Qualification by either company would be the strongest external validation AMEC has received, and would matter more for the equipment market than for either memory maker's output.

What would move this from evaluation to adoption is a disclosed tool order, which neither company has made. Until then, the reporting establishes intent to hedge. It does not establish a change in either fab's tool set.

Linked stocks: 005930 KS, 000660 KS, 688012 CH

先聲 First Word: Exclusives from Chinese-Language Sources

Shenzhen spot DRAM prices jump up to 14% in one week

Huaqiangbei's weekly DRAM quotes, released 4 Aug, ended roughly six months of flat trading: DDR4 8Gb 3200 rose from US$19.5 to US$22 (+12.82%), while DDR5 24Gb and DDR5 16Gb both rose 14.29% to US$48 and US$40. Spot is the channel tier, so the shortage has now moved past long-term contracts into retail distribution, which reads through to Nanya, Winbond, ADATA, Transcend and Team Group. (05 Aug 2026) Source: 華強北 DRAM 價噴漲 現貨單周強彈14% 南亞科、華邦等受惠

Fositek's AI components overtake foldable phones in one year

AI server rails and liquid cooling quick connectors rose to 55.7% of Fositek's 1H26 revenue from 19.2% in 2025, while foldable phones fell from 71% to 38%; 1H26 revenue was NT$7.92bn, up 62.6% YoY, with gross margin up 9.96 points to 33.13%. Management plans to double AI rail and quick connector capacity by 2027 from a current 3m connectors and 35,000 rail sets a month, both close to full. (05 Aug 2026) Source: 《電零組》富世達下半年營運樂觀 啟動擴產拚AI相關產能倍增

Tong Hsing's 800G optical customer clears a North American hyperscaler

Tong Hsing said the end customer for its 800G optical transceiver modules has passed qualification with a large North American cloud service provider, completing plant visits and supply chain verification, and shipments are now stable. The company guides 3Q26 revenue up a mid-single-digit percentage QoQ and gross margin toward a 30% to 35% target, above its long-run 25% to 30% band; 2Q26 gross margin was 31.1% and net profit rose 639% YoY. (05 Aug 2026) Source: 同欣電法說會/今年營運已恢復疫情前季節性走勢 AI 布局逐步開花結果

© 2026 Zero One Investment Research Pte Ltd. For informational purposes only. Not investment advice.