Nanya Tech Q1 2026: Legacy DRAM Squeeze Confirmed, and Three NAND Rivals Just Bought Equity to Secure Supply

Executive Summary

- ●Nanya Technology reported Q1 2026 revenue of NT$49.09B, up 63.1% QoQ and 582.9% YoY, with gross margin of 67.9% and EPS of NT$8.41 — a single quarter that earned roughly 4x the company's entire 2025 profit.

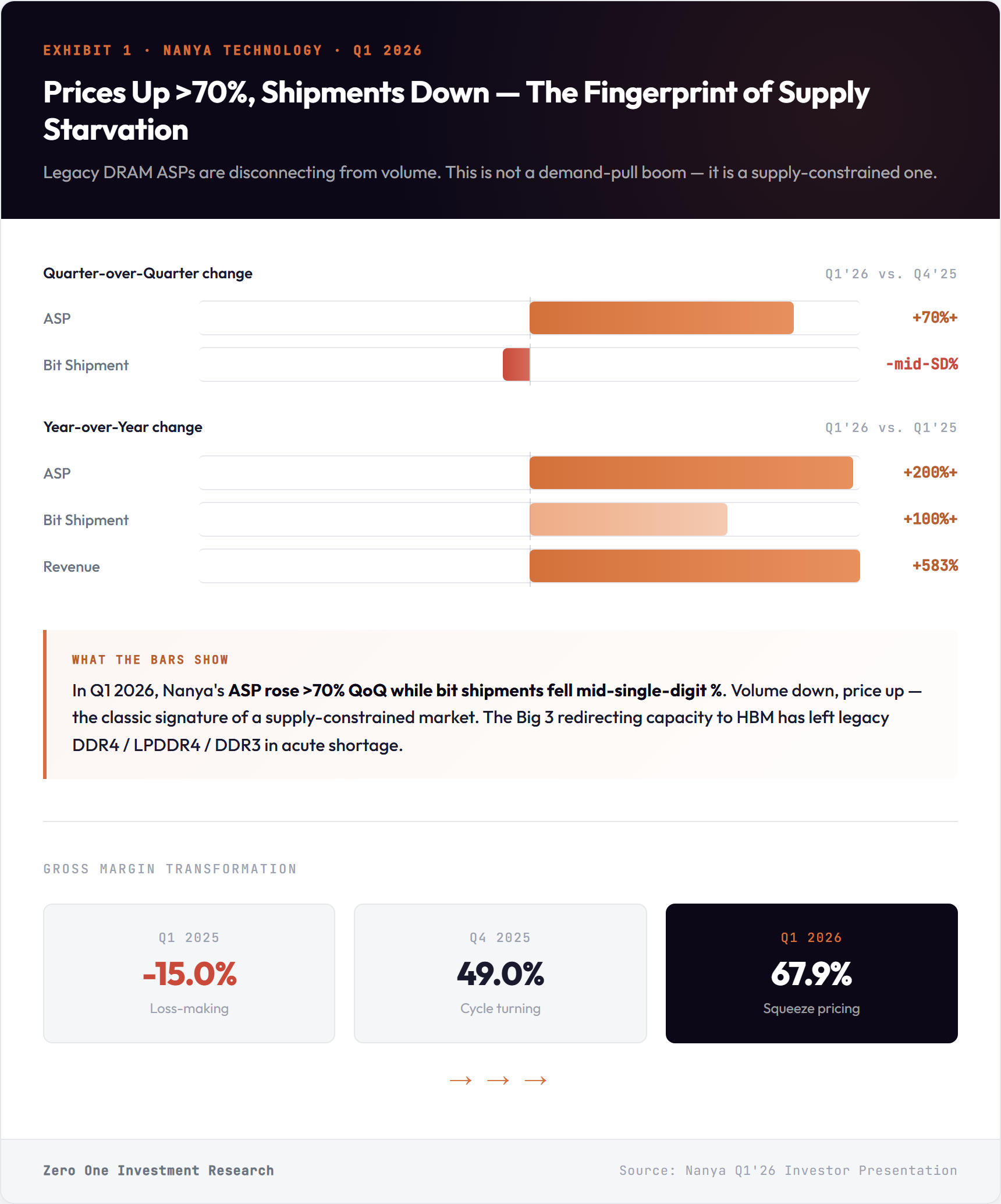

- ●The underlying signal is not HBM. Nanya is a legacy DRAM house (DDR4 / LPDDR4 / DDR3), with DDR5 at only 10% of revenue. Q1 ASPs rose >70% QoQ and >200% YoY while bit shipments actually fell mid-single-digit percent QoQ — pure supply-constrained pricing.

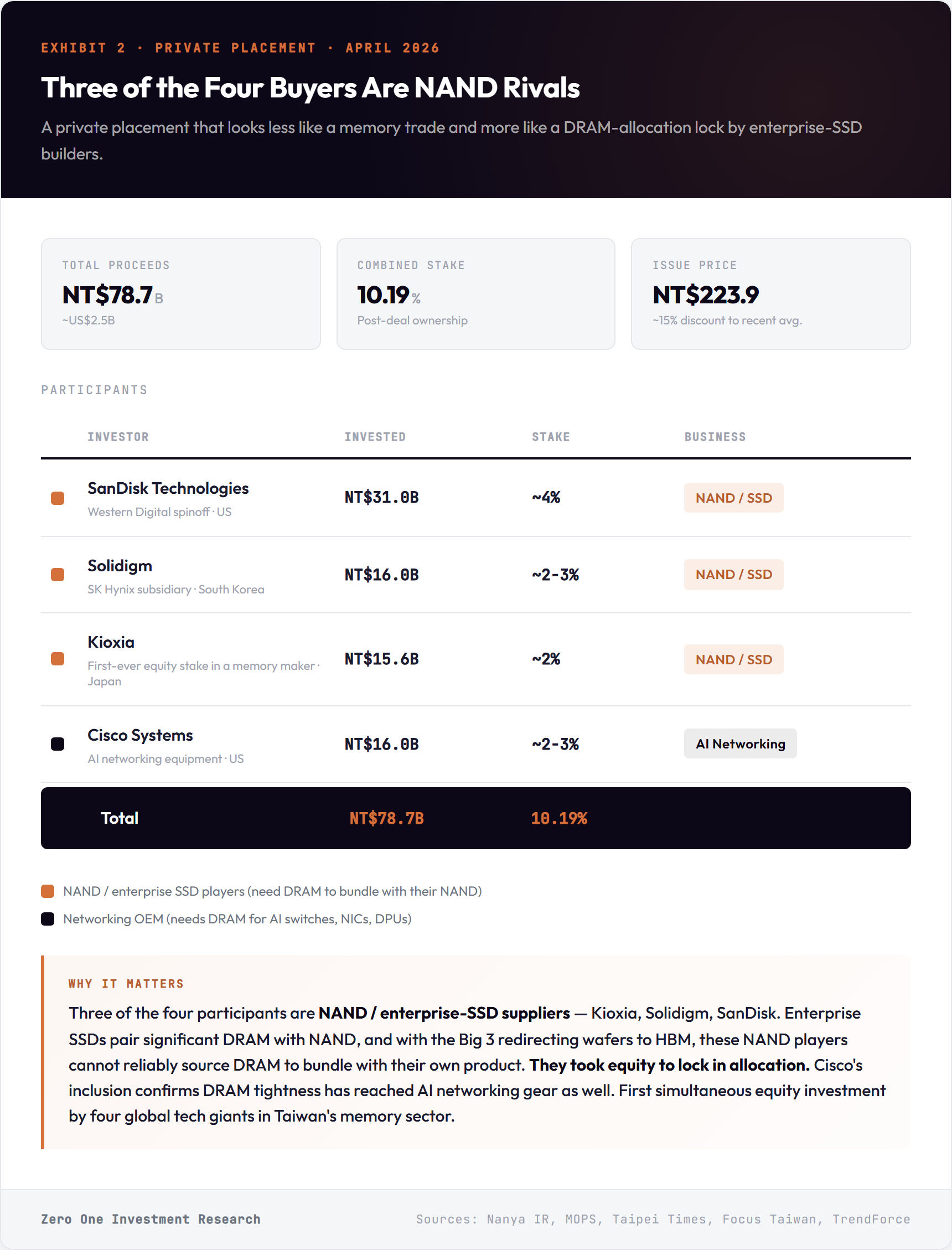

- ●The NT$78.72B private placement that closed April 8, 2026 now has named participants: SanDisk (~4%), Solidigm / SK Hynix (~2-3%), Kioxia (~2%), and Cisco (~2-3%) — collectively 10.19% of Nanya post-deal. Three of the four are NAND / SSD players. This is reportedly Kioxia's first-ever equity investment in a memory manufacturer, and the first simultaneous equity investment by four global tech giants in Taiwan's memory sector.

- ●Management explicitly said the company "cannot 100% satisfy market demand this year," guided Q2 2026 ASPs up double-digit % sequentially on top of Q1's +>70% move, and expects scarcity to extend into 2027. 2026 CapEx guided to ~NT$52B, roughly 4x 2025.

The print is real, but the narrative is different from "AI memory"

Q1 2026 revenue came in at NT$49.09B, a 63.1% QoQ and 582.9% YoY increase. Gross margin expanded to 67.9% from 49.0% last quarter and from -15.0% a year ago. Net income was NT$26.06B for EPS of NT$8.41. For context, Nanya earned NT$6.61B in all of 2025 — a single quarter now prints roughly 4x the prior year.

The temptation is to lump this into the general "AI / HBM memory boom" narrative. That would be a misread. Nanya does not make HBM. DDR5 is only 10% of revenue. The majority of the mix is DDR4, LPDDR4, and DDR3 — products that Samsung, SK Hynix, and Micron have been deliberately underinvesting in to redirect wafers toward HBM and high-density DDR5 for AI servers.

ASP up >70% QoQ on shipments that fell

The QoQ bridge is what tells the real story:

- ASP: +>70% QoQ, +>200% YoY

- Bit shipment: –mid-single digit% QoQ, +>100% YoY

- FX: +low-single digit favorable QoQ

Shipments down, ASP up >70%. That is the fingerprint of a supply-starved market, not a demand-pull boom. Nanya's outlook slide is explicit: "DDR4 / LPDDR4 serving industry-wide supply gap" and "constrained DDR5, DDR4, LPDDR4 and DDR3 supply leads to legacy DRAM EOL." President Lee Pei-ing told analysts Nanya "cannot 100% satisfy market demand this year" and guided Q2 2026 ASPs up double-digit % sequentially on top of the Q1 move. Management expects the supply gap to extend into 2027.

The private placement identities tell you what is actually tight

The NT$78.72B (~US$2.5B) private placement that closed on April 8 has been disclosed by participants. Shares were issued at NT$223.9, roughly a 15% discount to recent averages. The placement is reportedly Kioxia's first-ever equity investment in a memory manufacturer, and the first simultaneous equity investment by four global tech giants in Taiwan's memory sector.

Three of the four participants are NAND / SSD players. This is the detail that changes the read. Enterprise and cloud SSDs pair significant amounts of DRAM with NAND (DRAM handles temporary data before it is written to NAND), and DRAM shortage since late 2025 has made it hard for NAND-focused suppliers to bundle complete SSDs for hyperscaler customers. Taking equity in Nanya — and signing supply agreements spanning DDR5, LPDDR5, DDR4, and RDIMM — is a way for them to lock DRAM allocation in a market where the Big 3 are redirecting capacity to HBM.

Cisco's participation is the other interesting data point: DRAM for AI networking equipment (high-port-count switches, smart NICs, DPUs) is apparently tight enough that a systems vendor will take equity in a Taiwanese DRAM maker to secure supply.

Equity stakes by customers in their own DRAM supplier are not routine commercial behavior. Historically we have only seen similar patterns in upstream specialty materials or when buyers are worried about structural scarcity rather than cyclical tightness.

The industry capacity response is a 2027 event

Nanya guided FY26 CapEx to ~NT$52B, roughly 4x the NT$13.4B spent in 2025, with WFE at ~30% of total (implying ~NT$15.6B of WFE spend at Nanya alone). Equipment move-in at the new fab is targeted for Q1 2027, with 1C / 1D / EUV development "on schedule." Bit shipments are guided up teens% YoY for 2026.

2026 is locked in as a tight-supply year. Management stated Q2 will "further improve beyond Q1" and that "high gross margin is sustainable in the next few quarters."

Take-aways for the broader supply chain

### Big 3 DRAM: Samsung, SK Hynix, Micron

Our read: Nanya's print is the externally visible version of what is already happening inside the Big 3. All three have extended DDR4 lifecycles, are redirecting wafers to HBM at a roughly 3:1 consumption ratio, and are publicly admitting they cannot meet demand. Nanya is the cleanest pure-play proxy for the legacy side of that shift.

- Micron disclosed on its FQ1 2026 call that it can fulfill only ~55-60% of core customer demand and named three structural drivers: AI data center buildouts, HBM's 3:1 wafer consumption vs. DDR5, and multi-year cleanroom lead times. Its DDR4 ASPs rose up to 50% QoQ in the "legacy rally." Micron also signed an LOI in January 2026 to acquire PSMC's P5 fab (~US$1.8B) to add DRAM capacity — a direct response to the same supply gap driving Nanya's ASPs.

- Samsung and SK Hynix have both extended DDR4 production into 2026 rather than EOL as originally planned, because DDR4 has become an "unexpected cash cow." SK Hynix said on its October 2025 call that HBM, DRAM and NAND capacity is "essentially sold out" for 2026. Samsung is targeting a ~47% lift in HBM wafer output to 250k WPM by end-2026. HBM expansion and legacy DRAM tightness are mutually reinforcing.

- The Solidigm (SK Hynix subsidiary) participation in the Nanya placement also signals that even the world's #2 DRAM maker is comfortable outsourcing legacy DRAM supply for its NAND / SSD business — tacit validation that internal allocation is going to HBM.

### Other Taiwan legacy DRAM: Winbond, PSMC

Our read: The Taiwan legacy DRAM cohort is in the same squeeze, and their own management commentary is arguably more aggressive than Nanya's on pricing. Winbond is telling the market prices could rise nearly 4× by mid-2026. PSMC's exit from legacy foundry memory amplifies the shortage.

- Winbond publicly expects DRAM prices to rise ~90-95% in the current quarter and continue in similar magnitude next quarter — cumulatively approaching 4× higher by June 2026. Its 2027 DRAM capacity is already pre-sold, 2026 CapEx is set at a record NT$42.1B, and management is targeting NT$100B in consolidated revenue. Directionally identical to Nanya, at a different Taiwan legacy DRAM supplier.

- PSMC sold its P5 fab site to Micron in January 2026 and is effectively exiting legacy DRAM foundry work — removing legacy capacity from the market. PSMC's own Q3 2025 self-produced DRAM revenue was already up 62.8% QoQ before the major pricing surge hit.

### Wafer Fab Equipment: AMAT, Lam Research, ASML, TEL

Our read: Nanya alone is adding ~NT$39B of incremental CapEx YoY with a new fab build. Layer in Winbond's record NT$42.1B, Micron's P5 ramp, and Samsung / SK Hynix's HBM expansion, and 2026-27 memory WFE is a materially stronger setup than consensus has been modeling.

- Industry WFE is projected to expand ~9% in 2026 to ~US$135B, with memory (DRAM and HBM) called out by Applied Materials, Lam, and KLA as among the fastest-growing segments.

- Lam Research has disclosed multiple critical etch wins at a major DRAM manufacturer with its Akara 3D-DRAM etch system, plus Aether dry-resist selected as production tool-of-record at a leading DRAM customer — direct indications that memory WFE bookings are translating into revenue.

- Applied Materials management has explicitly named DRAM and HBM as fastest-growing WFE sub-segments for 2026.

- Nanya's ~NT$15.6B WFE spend at one second-tier memory player is a non-trivial incremental data point when extrapolated across the legacy-DRAM capacity response now underway.

### Enterprise SSD ecosystem: SanDisk, Kioxia, Solidigm

Our read: The private placement is functionally a DRAM-allocation contract dressed up as equity. Enterprise SSDs require meaningful DRAM as cache / buffer alongside NAND, and high-capacity SKUs are already reportedly facing year-long delays because the DRAM needed to complete them cannot be sourced. Three NAND players writing US$2B of equity checks to a Taiwanese DRAM maker is the clearest external signal of that bottleneck.

- SanDisk (~US$1B), Kioxia (~US$500M) and Solidigm (~US$500M) collectively invested roughly US$2B for ~8% of Nanya combined. Each signed long-term DRAM supply agreements. Kioxia's stake is reportedly its first-ever equity investment in a memory manufacturer.

- TrendForce has reported that high-capacity enterprise SSDs are hitting year-long delivery delays because Samsung, SK Hynix, and Kioxia are running NAND fabs flat-out but are DRAM-constrained on the bundle side. Expect enterprise SSD pricing and lead times to stay elevated through 2026 — positive for pricing at SanDisk, Kioxia, Western Digital exposures; cost headwind at hyperscaler storage tiers.

### AI networking: Cisco, Arista, and merchant silicon downstream

Our read: Cisco's participation is the least obvious but most interesting signal for investors. It confirms DRAM tightness has reached the control-plane, packet-buffering, and embedded-storage layers of AI switches — and Cisco is willing to take equity in a Taiwan DRAM maker to protect its ramp.

- Cisco's own commentary around its G300 AI networking chip and AgenticOps rollout has acknowledged that rising DRAM prices are feeding into gross margin guidance. Analysts have flagged this as a near-term margin risk against the AI networking revenue ramp.

- For Arista and other merchant-silicon-driven networking OEMs without an equity lock at a DRAM supplier, the read-across is negative on gross margin unless they can pass through pricing to hyperscaler customers.

### Hyperscalers and system OEMs

Our read: DRAM cost inflation is now a cross-stack issue, not an HBM-only issue. DDR4 / LPDDR4 / DDR3 ASPs are re-rating simultaneously with HBM and DDR5, compressing margins across the AI server bill of materials — memory, e-SSDs, NICs, BMCs, and switch gear — all at once.

- Hyperscaler capex has driven the HBM / DDR5 boom, but the second-order effect is that the entire memory stack is repricing. Watch for commentary on memory cost pass-through, system ASP increases, and any slippage in AI capex cadence from the CSPs in Q2 2026 prints.

### Nanya's own non-commodity option: UWIO

Our read: A small but strategically interesting footnote — Nanya's "customized AI UWIO memory" is their attempt to escape the pure commodity DRAM label. Initial revenue only, but worth tracking as non-commodity optionality through 2026-27.

- Ultra-wide I/O is a niche custom memory format aimed at AI inference and edge applications. Nanya disclosed initial revenue contribution in Q1. Material upside would require meaningful design wins with AI silicon vendors, which the private placement partners may help accelerate.

Bottom line

Nanya's Q1 print is the clearest public data point yet that the AI capex cycle's second-order effect — starving legacy DRAM of capacity — has produced a pricing environment dramatic enough to change capital structures. A 67.9% gross margin at a non-HBM, non-leading-edge DRAM maker, combined with three of its customers' NAND rivals and a major networking OEM taking equity stakes to lock in supply, is the signal. Bit shipments actually fell QoQ while ASPs ran up >70%. Management says they cannot satisfy demand this year and expect scarcity into 2027. For investors, the more interesting exposure vectors are (i) other legacy DRAM beneficiaries, (ii) WFE names serving the resulting capacity response, and (iii) cost-side pressure points in the AI server, enterprise SSD, and AI networking stacks.

Related Research

TSMC 2Q26 Earnings: Full-Year Growth Guided to Slightly Above 40%, Ahead of the Street

TSMC beat every guided line in 2Q26 and raised FY26 revenue growth guidance to slightly above 40% in US dollar terms, above pre-print consensus, with the capital budget lifted to US$60-64bn and US$100bn more committed to Arizona.

Read more SemiconductorsNanya's Shortage Extends Through the Second Half

Nanya posted record 2Q26 revenue of NT$82.55bn (+68% QoQ) at a 79.5% gross margin, and guided the third quarter to improve further, refuting the sequential decline consensus had modelled.

Read more SemiconductorsASML 2Q26 Preview: Consensus Sits at the Top of the Full-Year Guide

ASML reports 2Q26 on 15 July. Street revenue of EUR40.0bn for the year sits at the top of the EUR36-40bn guide, and the print arrives without the quarterly bookings number the market used to lean on.

Read more